TRADE & ECONOMY

The Government of Pakistan has directed the Federal Board of Revenue (FBR) not to raise import taxes and duties on goods coming from several key countries, including the United States, China, the United Kingdom, Germany, France, and Japan, FBR sources confirmed on Wednesday.

According to officials familiar with the matter, the Ministry of Finance opposed any tax hikes during ongoing tariff negotiations with the United States, which had earlier increased tariffs on Pakistani products in response to Pakistan’s own import taxation policies.

With crucial trade, tariff, and investment discussions between Pakistan and the US likely to be held in July, the decision aims to create a more favorable environment for diplomatic and economic negotiations.

Germany, which has been Pakistan’s leading development partner in alternative energy projects, is also exempted from any import tax increases. Officials say maintaining stable trade terms with Berlin is essential for the continuation of joint renewable energy initiatives.

As for the United Kingdom, sources note that it remains Pakistan’s largest export destination outside the European Union, and has been actively seeking new trade partners post-Brexit. Stable tax policies are expected to further encourage UK-Pakistan trade flows.

Regarding China, FBR officials emphasized that import and e-commerce-related taxes have been deliberately kept low due to the integral role Chinese goods play in supporting local businesses and employment. A significant volume of imported goods feeds into Pakistan’s retail and wholesale sectors, contributing to job creation.

Trade analysts see this move as a balancing act by the government, trying to preserve global trade partnerships while safeguarding domestic business interests. The decision also comes amid a backdrop of rising inflation and economic uncertainty, where any increase in import costs could further burden consumers and manufacturers.

Sources confirmed that all relevant stakeholders—including the Ministry of Commerce and the Board of Investment—are aligned on ensuring no disruptions in trade flows, particularly ahead of sensitive bilateral negotiations with major partners.

-

Pakistan, US Set to Conclude Trade Talks Next Week...

Pakistan & US to wrap up trade talks next week after Aurangzeb-Lutnick virtual meet. Strat...

-

Sindh, Balochistan Assemblies Approve Budgets for ...

Sindh okays Rs 3.45tr budget with tax relief in health, agri, transport & entertainment; j...

-

Pakistan, UAE Sign Deals on Visa-Free Entry, AI & ...

Pakistan & UAE ink deals on visa-free diplomatic entry, AI, & joint investment task force ...

-

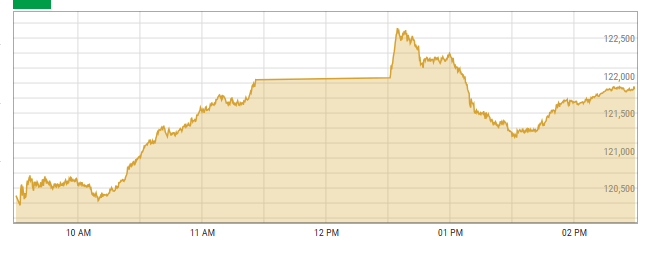

PSX Soars Over 6,000 Points as Ceasefire Cools Ira...

PSX surges 6,079 points after Trump announces Iran-Israel ceasefire. Market halts triggere...

-

Prof. Magsi Rejects Budgets, Slams Cuts to Univers...

ASA President Prof. Amjad Magsi rejects federal & Punjab budgets, says public universities...